i agree with needing more ways to increase total TVL but i don’t think we should allow NFTs on the collateral side.

This is turning into a very hot topic, using LP tokens for instance as collateral, and moving first in this could be a pretty significant upset to emerging projects. Full support.

1 Like

I raise my hands in favor!

This is a very good growth point. I believe that the Bond Pool will greatly increase the TVL and market cap of Wing.

Especially looking forward to it!

1 Like

Yes it’s kind of hard to collateralize NFTs with oracle.

A feasible solution is using a convertible note agreement.

For example: Alice wants to borrow money from Wing community using NFT A. Alice opens an NFT A - USDT contract. Bob, Charlie, and David noticed this contract. After doing research and viewing the underlying artwork behind NFT A, these three bidders give the following bids:

Bob: 200 USDT

Charlie: 500 USDT

David: 800 USDT

David wins the bid and his 800 USDTs are locked in the contract. Alice can withdraw 800 USDT by locking NFT A. Alice pays interest to David while the contract is active. Under certain circumstances:

- Alice fails to pay interest

- Alice actively defaults at any time

- Alice fails to pay 800 USDT when the contract ends

David can get NFT A + interests accrued in the contract.

This is similar to a convertible bond, except that the borrower has the right to decide whether to pay back the loan or transfer the ownership of NFT to the lender.

1 Like

The whole bond pool idea is great.

I agree with including NFTs into bond pool.

A few questions:

1 WING distribution mechanism. Does lender and borrower receive WING incentive? If so, on what base?

2 Risk control problem. What if no one buy the collaterals in the default auction, who will take the loss? Will there be a insurance part or auditing part to participate?

3 How can Wing project earn profit from the pool? Still charge 15% of interests?

4 Any candidates?

1 Like

I have some questions:

- Are there already any candidate bond issuer and bond buyer?

- Have you considered the maturity and interest rate of the bond in band pool?

- I am also worried about the issue of risk control. In real life, there are third-party rating agencies, it is important to control the risk.

- Will the band pool share WING’s incentives? Will it reduce the WING APY of the flash pool?

All issues need to be considered before going on the band pool.

This is a proposal to include OST as a collateral asset.

- Who is the interested party for this collateral application?

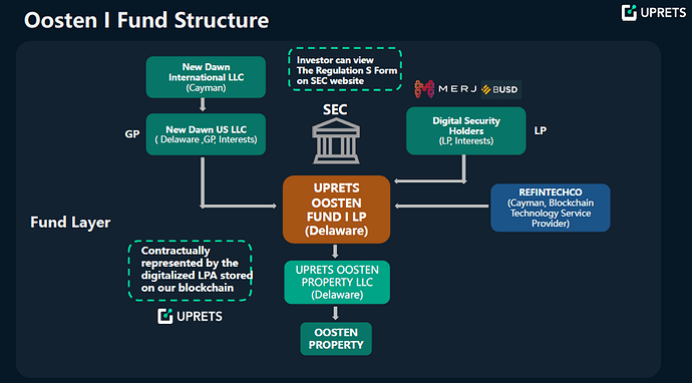

The asset originator, New Dawn US, is represented by Ryan (ryan@newdawn.io, Managing Partner at New Dawn) and Jake (jake@newdawn.io, Managing Partner at New Dawn).

UPRETS is providing the digital security issuance technology and framework for bringing real estate assets to MCD. The main contact for the application is Ran Wei (ran@uprets.io) of UPRETS as well as Wesley Ma (Wesley@uprets.io).

- Provide a brief high-level overview of the project, with a focus on the applying collateral token.

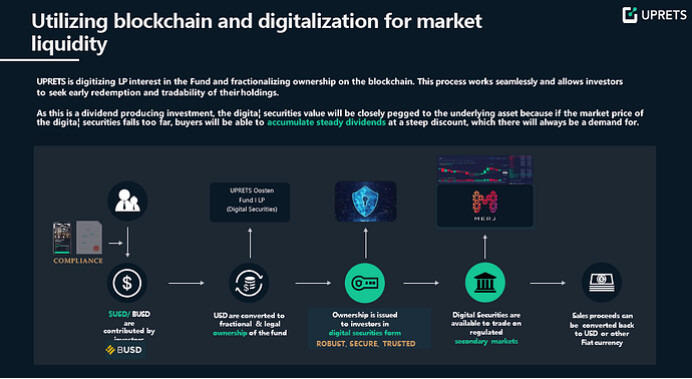

OST is asset-based digital securities based on advanced digitalization technology designed for global real estate investors and blockchain enthusiasts. With offices in New York, Dubai and Beijing, entwined with its extensive range of strategic partnerships, the international digitalization platform UPRETS aids in developing the non-fungible tokens to create a legally compliant real estate financial product available for investors with revolutionary spirits. Secondary trading on MERJ Exchange further facilitates KYC/AML, market assurance and trading liquidity. For more information, go to https://www.uprets.io/#/events/merj.

The Omnilayer & self-owned patented consortium chain Xbolt secures the OST digital securities structure and its compatibility to mainstream public chain and secondary exchanges and enables support payment with FIAT and BUSD. The ownership is issued to investors in a robust, secure and trusted digital securities form to accumulate steady dividends at a steep discount, which there will always be a demand for global real estate investors.

- Provide a brief history of the project.

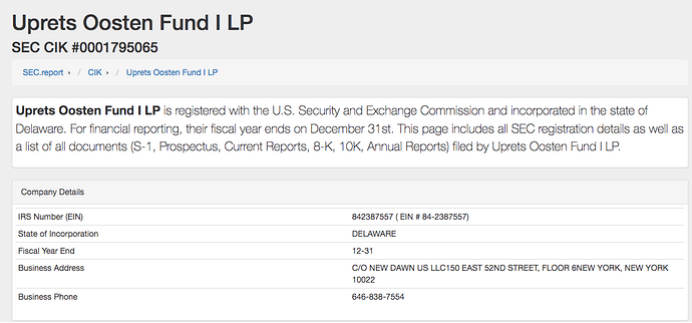

OST is the phase I legally compliant digital securities of the Oosten project, corresponding to the limited partnership interest of UPRETS Oosten Fund I LP, a real estate fund company located in Delaware, USA that holds the apartment No.730. UPRETS Oosten Fund I LP was completed through private equity investment on March 13, 2020, in compliance with the U.S. SEC’s Reg D and S standards, and simultaneously issued 100 million corresponding OST digital securities through the digitalization technology platform, UPRETS, and was listed on the MERJ Exchange on June 5, 2020, and opened the first transaction on June 25, 2020.

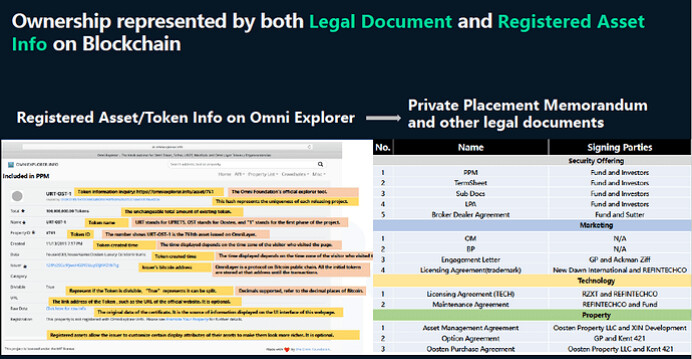

- Link to the whitepaper, documentation portals, and source code for the system(s) that interact with the proposed collateral, and all relevant Ethereum addresses. If the system is complex, schematic(s) are especially appreciated.

Website:uprets.io

OST Contract Ethereum Address: 0x6cF9Cc747026945654b596a6a14a675347C2FD70

OST and Oosten Property Brochure: (English ver.) https://github.com/FAN-finance/Description_OST/blob/main/OST%20Brochure_en.pdf

(Chinese ver.) https://github.com/FAN-finance/Description_OST/blob/main/OST%20Brochure_cn.pdf

UPRETS OOSTEN FUND Formation Documentation: https://github.com/FAN-finance/Description_OST/blob/main/UPRETS%20OOSTEN%20FUND%20Formation.pdf

Oosten Property Purchase Agreement: https://github.com/FAN-finance/Description_OST/blob/main/Oosten%20Property%20Purchase%20Agreement.pdf

Limited Partnership Agreement (Executed): https://github.com/FAN-finance/Description_OST/blob/main/Limited%20Partnership%20Agreement_Executed.pdf

LP Subscription Agreement (Executed): https://github.com/FAN-finance/Description_OST/blob/main/LP%20Subscription%20Agreement_Executed.pdf

Wrapper OST (wOST) Contract Address: 0x4c17f7abdbf507f7f18113faf01fd78c94d60090

- Link any available audits of the project. Both procedural and smart contract focused audits.

Audited by EY.

- Link to any active communities relating to your project.

LinkedIn: https://www.linkedin.com/company/14482223

Facebook: fb.me/uprets2019

Twitter: https://twitter.com/uprets_io 1

Medium: https://medium.com/uprets

- How is the applying collateral type currently used?

Our collateral which is the OST Digital Securities represents the limited partnership interest in UPRETS Oosten Fund I LP that is being traded on MERJ Exchange and used for enjoying the steady dividend return of the rental revenue and value appreciation of the underlying asset. We have taken the real estate property digitalized with our UPRETS integrated digitalization resolution that activates its liquidity and ensures its security and manageability. The value of each token is firmly backed-up by the assets, and determined by the current price on the MERJ Exchange.

- Does one organization bear legal responsibility for the collateral? What jurisdiction does that organization reside in?

UPRETS Oosten Fund I LP, which was registered and in legal compliance with the U.S. SEC’s Reg D and S standards, which are securely developed based on the Xbolt consortium chain that regulatorily issued on the Omnilayer, bear the legal responsibility for the collateral. Involved third-party law firms, which include Baker&McKenzie, O’Melveny&Myer and Dahui, will ensure the documentation and any related legal circumtances’ rights and liabilities.

- Where does exchange for the asset occur?

OST was listed on the MERJ Exchange on June 5, 2020, with an initial market value of US$1 million and an initial price of US$0.01 per OST. Investors who have obtained digital securities through first-level fundraising have successively transferred their OST to MERJ, and conducted the first transaction on June 25, 2020.

MERJ Exchange is the only registered exchange in the Seychelles. As a regulated market, MERJ Exchange is regulated by the Seychelles Financial Services Authority and the Central Bank of Seychelles that follows the same exchange standards as other mainstream exchanges, for instance, LSE, NYSE, Nasdaq, CBOE and CME. MERJ is a member of the National Numbering Agency (a joint organization that includes central banks, mainstream exchanges and monitoring agencies) and is the only token exchange among them. MERJ is also an affiliate member of the World Federation. As of July 16, 2020, MERJ has listed 43 securities. Since its listing, OST has achieved eight transactions and the bilateral transaction volume has reached 298,924 tokens.

- Has your project obtained any legal opinions or memoranda regarding the regulatory standing of the token or an explanation of the same from the perspective of any jurisdiction? If so, those materials should be provided for community review.

Further details can be retrieved from the aforementioned UPRETS OOSTEN FUND Formation Documentation, at: https://github.com/FAN-finance/Description_OST/blob/main/UPRETS%20OOSTEN%20FUND%20Formation.pdf

- Describe whether there are any regulatory registrations for the token and provide related documentation (including an explanation of any past or existing interactions with any regulatory authorities, regardless of jurisdiction), if applicable.

OST is a private offering by UPRETS Oosten Fund I LP, a Delaware limited partnership (the “Partnership”), of securities limited partnership interests (“LP Interests”) in the Partnership made in reliance on Regulation S (“Regulation S”) under the United States Securities Act of 1933, as amended (the “Securities Act”), solely to non-U.S. persons (as defined in Regulation S) who are outside of the United States (the “Regulation S Offering”). The limited partnership interests are expected to initially be issued in book entry form. At the election of the holder, the Partnership expects to tokenize the LP Interests in the form of uncertificated digital securities prior to the expiration of a distribution compliance period (in tokenized form, a “Token”, and LP Interests in book entry or Token form, a “Security”).

The Partnership is a newly organized Delaware limited partnership with no operating history and no material assets. The general partner of the Partnership is New Dawn US LLC, a newly formed Delaware limited liability company (the “General Partner”). Concurrently with the Regulation S Offering, the Partnership may undertake a private offering of Securities in reliance on Regulation D under the Securities Act (“Regulation D”) solely to U.S. persons (as defined in Regulation S) who are accredited investors (as defined in Regulation D) and who are in the United States.

Concurrently with the closing of the Regulation S Offering, UPRETS Oosten Property I LLC (“Oosten LLC”), a Delaware limited liability company and wholly-owned subsidiary of the Partnership, will purchase a one bedroom condominium unit (the “Property”) in a condominium development in the Williamsburg neighborhood of Brooklyn, New York, USA.

OST Digital Securities have not been and will not be registered under the Securities Act of 1933, as amended, or any other law or regulation governing the offering, sale or exchange of securities in the United States or any other jurisdiction. The securities offered in the Regulation S offering may not be offered or sold in the United States or to or for the account of U.S. persons (as defined in regulation S under the Securities Act) except pursuant to an exemption from the registration requirements of the Securities Act. This Regulation S offering is being made solely to persons who are not located in the United States and who are not U.S. persons (as defined in regulation S under the Securities Act) in reliance on Regulation S under the Securities Act. The issuer has not been, and will not be, registered under the investment company act of 1940, as amended.

No offers or sales of OST digital securities will be made in the People’s Republic of China or to PRC nationals or in any other jurisdiction where is its unlawful to sale or own the securities.

- List any possible oracle data sources for the proposed Collateral type.

All relevant self-captured Oracle data can be retrieved from: https://www.fan.finance/#/oracle. However, only partial essential data is presented at the front-end, if need, could ask for API portal to have access to all back-end database.

- List any parties interested in taking part in liquidations for the proposed Collateral type.

There will be two options depending on the volume:

Low to mid volume: The liquidation will be in addition to the above directed towards preferred global real estate investors and blockchain tech enthusiasts.

Mid to high volume: The liquidation will be through MERJ Exchange:https://merj.exchange/.

DeFi (Decentralized Finance): Use OST as the collateral and get liquidity in the FAN system: fan.finance.

- List the Wrapper Contract and Cross-Chain Contract Address:

Wrapper Contract: 0x4c17f7abdbf507f7f18113faf01fd78c94d60090

Cross-chain Contract: already developed and undergoing internal testing now. Will disclose detailed info in late May to early April.

1 Like

What is your target financing amount, interest rate and maturity?

- OST-1

- we can try 1 month

- Of course there are risks. Liquidation will be the biggest. If it’s a security token, then the issuance platform will be responsible for token wrapping and custodian

- Maybe

1 month, 200,000 USDT, 10% APY.

I think this is unnecessary. These special collateral assets can also be liquidated through Dutch auctions.

If this is an attempt, I think whether we should not go online in the secondary market at the beginning, because it is too complicated.

In my opinion, bTokens should not be partially fungible tokens. It should be OEP-4 asset, same bonds have the same bToken, and different bonds have different bTokens, like LP token on Sushiswap and Uniswap.

Yes Dutch auction is a good way.

I agree this is complicated in the beginning.

However, deploying a bToken secondary market is a long-term imagination. It’s somehow necessary because a stable price feed is needed without off-chain solutions. This secondary market can make bTokens more liquid, and enable users to adjust fixed-income positions.

How to distribute WING incentives for Bond Pool?

I suggest a trial run in the first phase and release 6 WINGs to the Bond Pool every day, so the total incentive is 180 WING. It will be divided equally between the bond issuer and purchaser, and distributed to each purchaser in proportion to the capital contribution. The released incentives will not compete with other pools for the time being, and will come from the unallocated WING generated during the Wing Creation Mining Multiplication Event due to rate adjustments.

I am more interested in the price reduction range and frequency of the collateral liquidation.

I suggest that the liquidation of Bond Pool should be a Dutch auction, similar to the Flash Pool repurchase auction. Specific rules: Starting from the day after the last maturity date, the collateral will be auctioned at increasingly higher discount prices. The starting price is 120% of the bond issuer’s total repayment. The daily discount is 1% until all assets are auctioned or the value becomes 0 after 120 days, at which time the auction will end.

How many OST-1 will the first bond issuer supply?

33,000,000. Around this

Quote the ideas of our Dev team.

1. Bond Pool Mechanism

Bond issuance

The bond issuance is carried out in four steps:

( 1) Asset get mortgaged or withdrawn

( 2) Bond gets minted

( 3) Listed for sale or sells on its own

( 4) Issuance completed

This results in either:

The issuance was successful and the bonds were all bought - OR

The issuance failed, only part of the bond was bought, and the funds were returned to all parties - OR

IF Part of the issuance was successful, the unsold bonds are automatically transferred to the issuer of the bonds

Asset mortgaging or withdrawal

The bond issuer must mortgage the assets before issuing bonds, with the collaterals can be returned at any time before the bonds are minted.

The assets that can be used as collateral are:

OEP-4 homogenized assets such as BTC / ETH / Stablecoins / tokens

Valuable OEP-5 assets.

Other valued bonds (OEP-8 assets) that have been mortgaged but not minted into bonds can be retrieved at any time. OEP-4 and OEP-8 asset bond Issuers can select the quantity when retrieving them. OEP-5 assets can only be retrieved individually.

Bond minting

After the bond issuer has pledged their assets, the bond will begin to be minted.

Bond format: Since there may be a need to raise a large amount of assets, the bond should be separable to be implemented by using an NFT in the OEP-8 format.

The bond issuer must select the type of bond to be issued, bond maturity, loan asset type, annualized coupon rate, bond coupon price, number of coupon periods, fundraising deadline, bond effective date, and redemption deadline.

Bond types are divided into mandatory redemption and negotiable redemption. Negotiable redeemable bonds can only use OEP-4 assets as collateral.

Bond maturity refers to the duration of the bond.

Bonds that have been minted but not yet sold can be directly destroyed to retrieve the collateral.

Bond sale

The bond issuer can choose to sell the bonds publicly in the Bond Pool or sell the minted bonds on their own. Bonds that have not been purchased cannot be transferred freely.

(1) Public sale

The issuer chooses to sell the bonds publicly and needs to pay a fixed amount of ONT to the Bond Pool as an issuance fee. The longer the duration of the public sale, the higher the cost. After the bond is purchased, the purchaser’s funds are transferred to the Bond Pool smart contract, and the bond NFT is transferred to the purchaser’s account.

(2)Self-sell

Self-selling is generally applicable to the directional issuance of bonds. A purchase whitelist will be set up. The bond issuer will copy the bond ID n and send it to the purchasers off-chain. After the purchasers pay, the funds will be transferred to the Bond Pool smart contract, and the bond NFT will be transferred to the purchaser’s account.

Issuance complete

Once the bond is purchased, it is considered to have been issued. If the bond is not completely sold to the buyer after being minted, or the ratio of the bond’s collateral value to the borrowing value falls below the minimum collateral rate during the issuance process, the bond issuance will fail. This results in the bond’s collateral being returned to the issuer and the funds sold being returned to the purchaser.

(1)Successfully issued

All the bonds have been sold, and the proceeds from the bond sales have reached the address of the issuer.

Failed to issue

There is a buffer period of no less than one day between the bond offering deadline and the effective start date, which is called the refund period. If a batch of bonds is not fully sold, or the ratio of bond collateral value to borrowing value falls below the minimum collateral rate, any user can initiate a refund and liquidation during this period of time. Refund liquidation means that both the issuer and the purchaser can withdraw the assets they have spent. Bonds in the state of refund and liquidation will no longer enter the interest accrual period. Since the existence of incompletely sold bonds is not conducive to the overall risk control, the Bond Pool will incentivize users who initiate refunds and liquidation.

For under-issued bonds, even if no refund clearing transaction is initiated during the refund period, the bond cannot enter the interest accrual period. Any user operation will trigger a refund settlement of this type of bond.

Subscribe

The user purchases the bond NFT at its face value on the exchange. The NFT is shared by the bond issuer and the subscriber, while not being able to be destroyed.

After the purchase is completed, the subscribed assets are transferred to the bond issuer and the subscriber can transfer the NFT to anyone for sale on the exchange.

Interest payment

For long-term bonds, the bond issuer needs to pay interest regularly during the bond duration. If the interest unpaid is overdue, the bond will enter a default liquidation process.

During the duration of the bond, the bond issuer is required to pay interest regularly and pay the principal when it matures. The holder of the bond can withdraw the proceeds generated by the bond at any time. After the bond issuer has paid all the principal and interest, the bondholder can withdraw the principal by destroying the bond.

Timed interest payment

When the bond is issued, after the issuer set up the interest period, smart contracts will calculate each interest payment . The issuer needs to pay a certain amount of interest within the period of each interest payment period, otherwise it will be deemed as a breach of contract.

If it is the last interest payment, the issuer can repay the principal and interest at the same time to redeem their collateral.

Bondholders’ exercise of negotiable redeemable bonds

For negotiable redeemable bonds, bond holders candestroy the bond to obtain collateral during the holder’s exercise period.

R edemption

After the end of the bond interest calculation (if it is a negotiable redeemable bond, then it is after the holder’s exercise period), the bond issuer can redeem its collateral, repay the principal and interest, and the NFT will be destroyed.

The bond issuer cannot redeem this in advance, but they can pay interest in advance.

Withdraw income and principal

If only interest can be withdrawn, the bonds will not be destroyed after the interest is accredited. If the principal and interest can be withdrawn, the bonds will be destroyed after the principal and interest are received.

Settlement of interest on bond transfer

The first version will not develop the bond’s secondary market, but it will be considered in the later version.

Since Bond Pool’s bonds are issued based on the blockchain and are expressed as partially homogenized assets, the bonds can be transferred freely. If the transfer is a bond within the duration, and the bond still has interest in the Bond Pool smart contract and has not been withdrawn by the current holder , at this time, if the bond holder transfers the bond, the undrawn interest will enter the original holder’s account, and will not be transferred to the new holder.

After the Bond redemption period expires, the bill defaults. At this time, the bond purchaser can obtain all the mortgaged assets and the NFT will be destroyed.

There are two cases which result in defaults: a failure to pay interest on time and a failure to redeem collateral on time.

For indivisible assets (OEP-5 and OEP-8 assets), after the issuer defaults, bondholders can initiate liquidation, conduct collateral auctions, and repay the principal with the amount obtained after the auction. The collateral auction adopts a “Dutch” auction, where the highest price, the lowest price and the duration are negotiated by creditors.

For divisible homogenized assets (OEP-4 assets), after the issuer defaults, any bondholder can trigger liquidation. The liquidation process will distribute all collateral evenly to all bonds.

OEP-4, OEP-5, and OEP-8 assets cannot be liquidated at the same time.

When the rights and interests of bondholders are damaged, they can be paid through insurance. The first version of the Bond Pool will not support the insurance function.

2 . WING Incentive Distribution

The first phase will be a trial version, with 6 WING tokens to be released to the Bond Pool every day, so the total incentive over 30 days will be 180 WING. It will be divided equally between the bond issuer and purchaser, and distributed to each purchaser in proportion to the capital contribution. The released incentives will not compete with other pools for the time being, and will come from the unallocated WING fund, created from the rate adjustment in the initial stages of Wing.

1 Like